![]()

WARNING ABOUT FRAUD

- We have detected the use of Soda Capital in fraud attempts where deposits are requested. Soda Capital never requests advance payments as a condition for granting loan.

- We request that you DO NOT make any deposits or provide information to anyone claiming to be a representative of Soda Capital, and if necessary, report to the competent authorities.

AVOID BECOMING A VICTIM OF CRIME

Bridge Loan: The Strategic Boost for Your Next Real Estate Development

In business and real estate development, time is just as valuable as capital. Many major projects stall not because they are unfeasible, but because there is a timing gap between the need to execute and the arrival of permanent financing.

That is where the Bridge Loan comes in: a financial tool designed to bridge that liquidity gap and keep the machinery moving.

What exactly is a bridge loan?

It is a short-term financing structure (usually 6 to 36 months) used while a permanent or long-term source of funds is secured.

The logic is simple: You have a project that needs capital now, but the final funding (whether a mortgage loan, the sale of assets, or the close of an investment round) will arrive months later. The bridge loan lets you operate in the meantime without losing project momentum.

Distinctive Features

Speed and Term

They are agile loans with short maturities.

Collateral

They are usually backed by the same asset being developed or acquired.

Cost

Because of the higher risk and immediacy, interest rates and fees are usually slightly higher than those of a traditional mortgage loan.

The Strategic Ally of the Real Estate Developer

For a developer, a bridge loan is more than just a loan; it is a value accelerator. Its operating mechanics are designed around the construction lifecycle:

Progress-Based Disbursements

Funds are released according to the project schedule, ensuring capital is used efficiently.

Interest-Only Structure

During the life of the loan, monthly payments usually cover interest only.

Flexible Exit

The principal is repaid at the end through:

- The sale of the units (apartments, retail spaces, offices).

Why Use Debt Instead of Pure Equity?

Lower capital requirement

You do not need to have all the money in the bank to start.

Faster return

By finishing the project faster, profits arrive sooner.

ROE optimization

It increases the return on your own capital.

Practical Case: The Power of Leverage

Let us analyze how smart debt impacts Return On Equity (ROE). Suppose:

- Total project sales revenue: $100

- Construction-related expenses (hard and soft costs): $75

- Required capital: $75

- In the first case, everything is funded with investor equity

- In the second case, $45 is funded with investor equity and a healthy $30 debt facility

- Debt cost: 20% annually

When profitability is viewed as return on equity (ROE), the result looks like this:

The results of these scenarios are as follows:

| Rubro | Caso 1: Todo con Capital | Caso 2: Deuda sana + Capital | Δ% |

|---|---|---|---|

| Ingresos Totales | 100.00 | 100.00 | |

| (-) Gastos Operativos Totales | 75.00 | 75.00 | |

| Utilidad Operativa | 25.00 | 25.00 | |

| (-) Costo Financiero | 6.00 | ||

| Utilidad antes de impuestos | 25.00 | 19.00 | |

| (-) Impuestos | 7.50 | 5.70 | |

| Utilidad Neta | 17.50 | 13.30 | -24% |

| Deuda | 0.00 | 30.00 | |

| Capital Inversionistas | 75.00 | 45.00 | -40% |

| ROE | 23% | 30% | 6% |

The table above shows that by taking on healthy debt and reducing investor capital requirements by 40% (from $75 to $45), net profit falls by only 24%, while profitability increases by 6 percentage points (ROE from 23% to 30%). A healthy bridge loan can improve the profitability of your real estate project!

Soda Capital: Tailored Bridge Loans

In traditional banking, processes are often rigid and slow. At Soda Capital we offer a structured bridge loan designed to match the reality of your project.

Requirements to Obtain a Bridge Loan

Executive Project

The Executive Project is the complete set of technical documents, drawings, and specifications that define with absolute precision how the development will be built. It is the translation of the architectural concept into instructions that can be executed on site.

Main components:

Architectural drawings

Floor plans, sections, elevations, and construction details at scale.

Engineering projects

Structural, plumbing and sanitation, electrical, and special systems (HVAC, gas, telecommunications).

Calculation reports

Technical justification for each structural system and installation.

Technical specifications

Materials, finishes, quality standards, and construction procedures.

Bill of quantities and budget

Work quantities, unit prices, and estimated total cost.

Construction schedule

Activity timeline with critical path (Gantt).

Renders and model

Visual representation of the finished product.

A solid Executive Project minimizes change orders on site, controls costs, and is an essential requirement for obtaining construction permits.

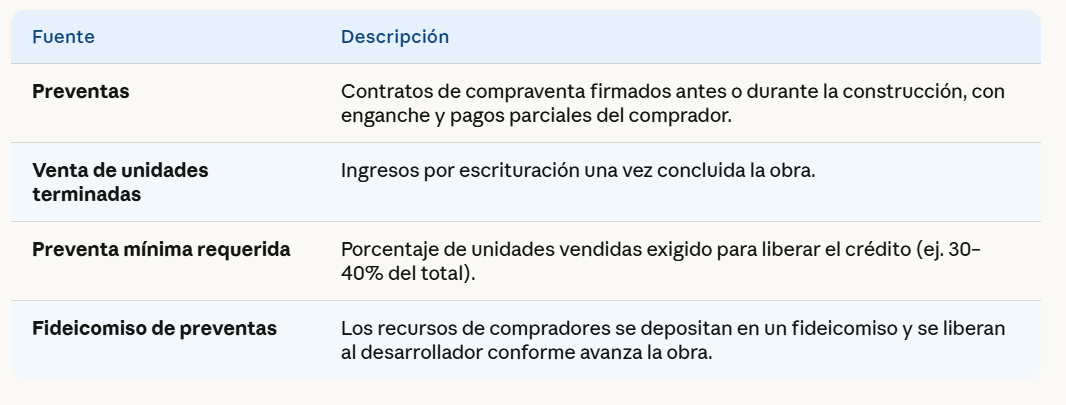

Clear Repayment Source (Pre-Sales / Unit Sales)

The repayment source is the specific mechanism through which the developer will generate enough revenue to cover the loan or investment received. It must be demonstrable, measurable, and have a defined schedule.

Most common structures:

Key indicators to demonstrate:

Sale price per m² vs. market price in the area.

Expected absorption rate (units/month).

Total amount of formalized pre-sales to date.

Cash flow projection with closing dates.

Legal Documentation for the Property and the Company/Individual

This item confirms that both the real estate asset and the borrower are legally established and in order to execute the project.

From the Property:

Notarized deed for the property with updated registry data.

Certificate of no liens (no mortgages, seizures, or litigation).

Property tax receipt up to date.

Land use compatible with the project to be developed.

Construction permit or proof of application.

Zoning and alignment certificate.

Environmental impact statement (if applicable).

From the Company (Legal Entity):

Articles of incorporation and amendments.

Current notarized powers of attorney for the legal representative.

Updated Tax Status Certificate (RFC).

Audited financial statements (last 2-3 years).

SAT registration and positive compliance opinion.

From the Individual (if applicable):

Valid official ID.

CURP and RFC.

Proof of address.

Tax returns for the last 2-3 years.

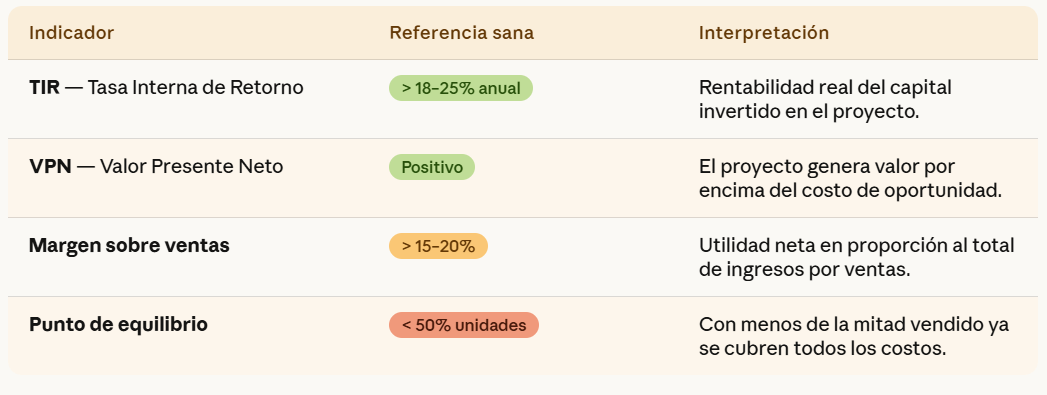

Project Feasibility Analysis

This is the study that determines whether the project is technically, financially, and commercially viable. It is the basis for the investment or credit decision.

Analysis dimensions:

Commercial Feasibility

Market study: supply and demand in the area, competitor pricing, target buyer profile.

Absorption analysis and estimated time to place units.

Product differentiators vs. the competition.

Financial Feasibility

Total required investment (land + construction + indirect costs + financing + operating expenses + commissions + administrative expenses + marketing).

Capital structure (debt vs. equity).

Revenue, expense, and cash flow projections.

Profitability indicators:

Technical Feasibility

The development team’s ability to execute the project.

Availability of contractors and suppliers.

Identified technical risks and mitigation plans.

Legal/Regulatory Feasibility

Confirmation of permitted land use.

Timelines for obtaining permits and licenses.

Legal risks related to the property or the company.

Do you have a project coming up? Let us help you structure the ideal financing so you can keep building.